A privacy layer between you and every merchant

Every online payment leaks your card number, name and billing address for merchants, processors and analytics tools to store. Halocard provides a protective layer in between, so merchants only see the details you choose to share. This is commonly known as payment-masking.

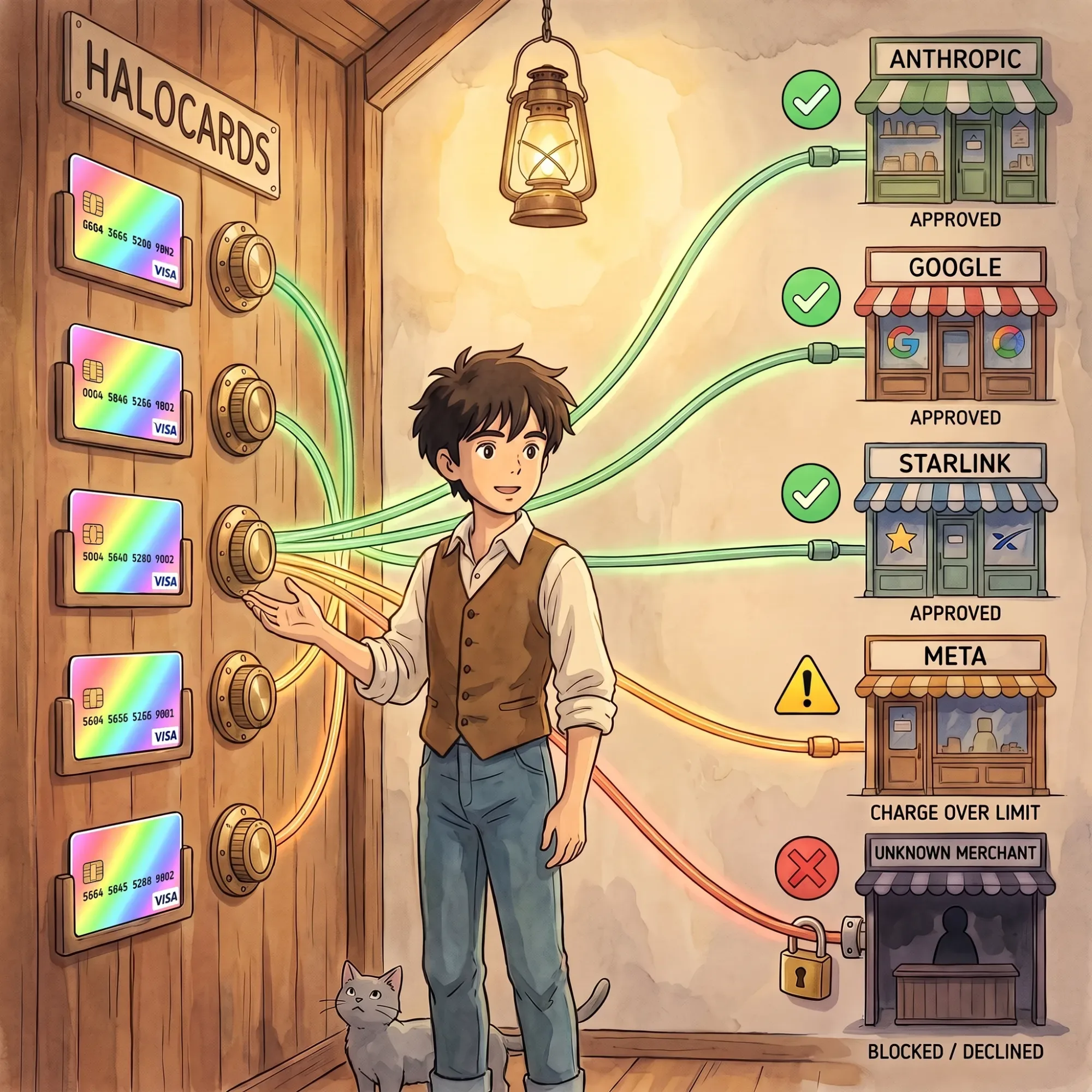

Lock, replace or cancel any card instantly

Spotted a charge you don’t recognise, or a merchant charging without your permission? Lock your card in a tap, or delete it and create a replacement in seconds. The new card keeps your shared balance while the old one stops working immediately.

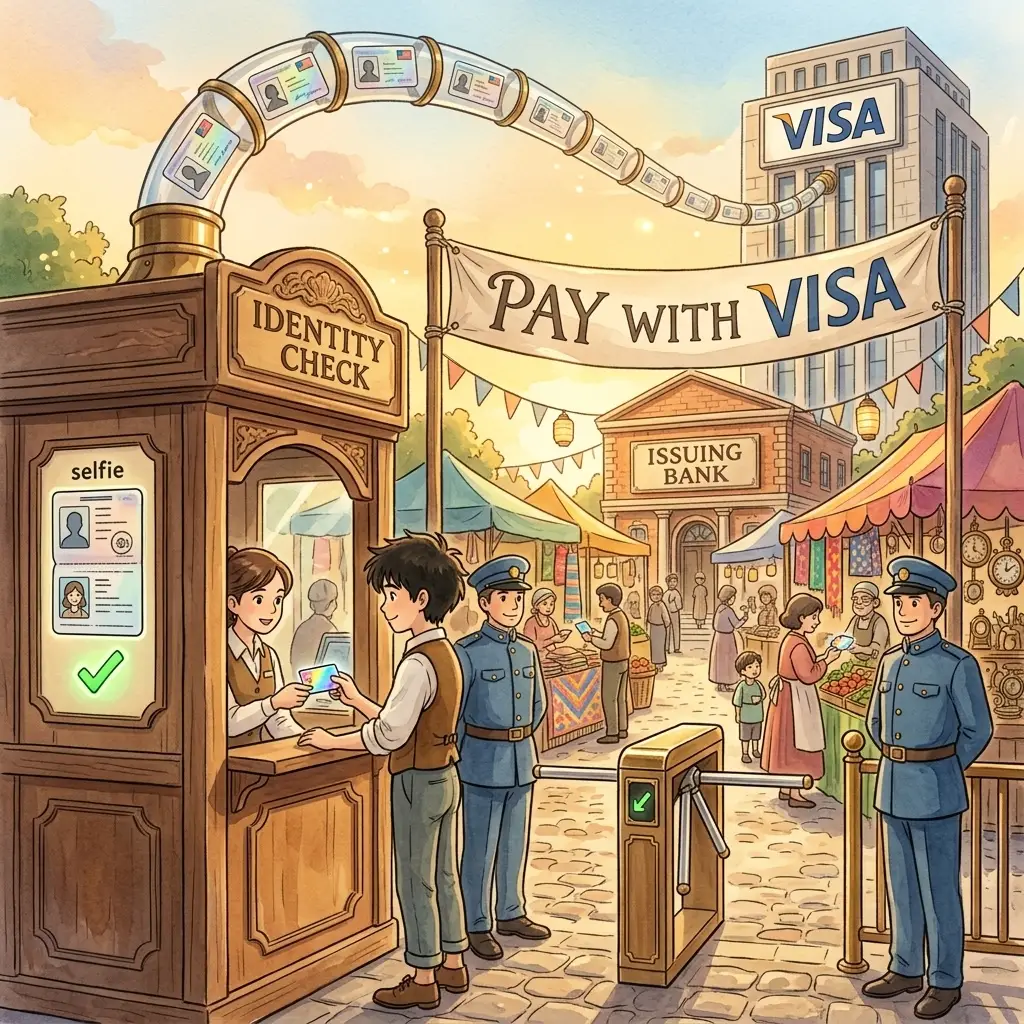

We verify essential details only

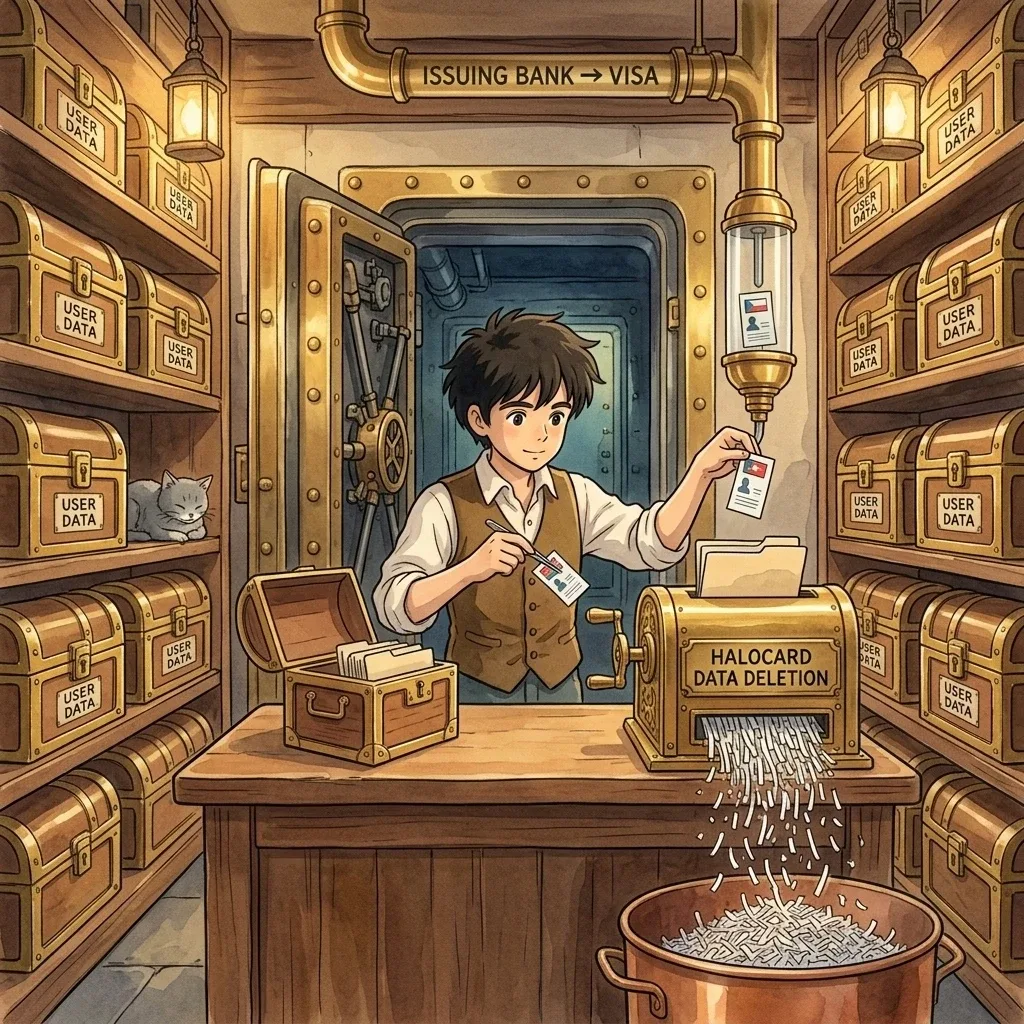

US consumer regulations require we confirm your identity before issuing a credit card, specifically: name, address, date of birth, government ID (and SSN for US residents). Your data is then permanently removed from our servers, although our identity verification provider (Sumsub) and Visa keep them for the period the regulations require.

Delete your account and data at any time

Close your account whenever you like and we permanently erase your data from our servers. Some records must remain with our regulated partners for legal and compliance periods, but for us, deletion means wiped and unrecoverable.

No card is truly private, but we minimise data exposure

Visa still sees the merchant, amount, date and location of every payment, the unavoidable price of a reliable card that works everywhere you need to use it. Within those constraints we minimise our role, mask what merchants see, and never sell or correlate your data.

We’re regulated and don’t provide anonymous cards

Halocard is a registered, US Money Services Business with the authority to issue cards on behalf of our issuing bank and Visa. Being regulated means we operate a legal and sustainable card program and do not provide anonymous or no-KYC cards that sit in legal grey zones that often get blocked, resulting in a loss of funds.