How to Choose the Best Virtual Card Provider for Your Business

Edward Taylor

-

The best virtual card provider for your business depends very heavily on your company's workflow, international payment requirements, software stack, and approval needs.

-

Different virtual cards will fit different teams, with some prioritizing accounting automation while others focus on merchant acceptance and global access.

-

Some of the most overlooked factors to consider are support quality, spending controls, onboarding friction, transaction fees, and hidden FX.

-

Before committing to any single virtual card provider, always run a small pilot using real business expenses, vendor payments, and recurring subscriptions.

This guide is designed to help SMB owners, finance teams, and founders objectively evaluate virtual card solutions based on their real operational needs. This article focuses on virtual cards, virtual corporate cards, and virtual credit cards designed for business spending, online payments, operational purchasing, and SaaS subscriptions. Let's discuss how to choose the best virtual card provider for your business.

The 7 Criteria That Matter When Choosing a Virtual Card Provider

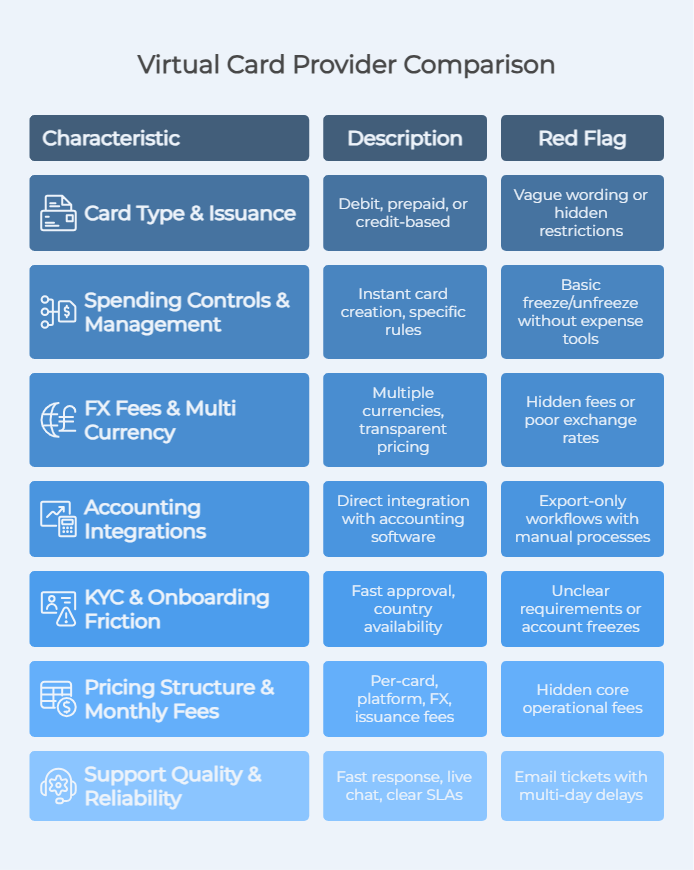

There are 7 criteria that matter when choosing a virtual card provider for businesses, with card type and the issuance model being one of the most important.

1. Card Type and Issuance Model for Virtual Cards

Not all virtual cards work the same way, as some providers issue virtual debit cards or prepaid cards, while others may issue true virtual credit cards that are tied to a secured balance or credit line. This is important because merchant acceptance varies.

Many international platforms, advertising networks, and SaaS vendors do not accept prepaid cards, whereas credit cards or traditional corporate cards are generally accepted. If your company relies heavily on global SaaS tools, recurring billing, or subscriptions, the issuance model is one of the most important factors to evaluate.

When you're looking for the best virtual card solution, look at several factors including:

-

Whether the cards are debit, prepaid, or credit-based

-

Country of issuance

-

BIN reputation and acceptance rates

-

Support for recurring billing and online purchases

Red flag: vague wording around card type or hidden restrictions tied to merchant approval.

2. Spending Controls and Card Management

Next, evaluate whether or not the virtual card has strong spending controls. After all, spending controls are one of the biggest reasons why companies adopt virtual corporate cards in the first place. The best virtual card platforms allow teams to instantly create cards, assign departments, set highly specific rules around usage, and freeze cards.

Good systems will make it easy to set spending limits, reduce fraud exposure from shared company cards, and track subscriptions. For growing businesses, the ability to issue unlimited virtual cards is also valuable, because instead of one shared card across multiple vendors, each employee or tool can receive dedicated card details with tailored controls.

Look for:

-

Per-user restrictions

-

Merchant category restrictions

-

Time-based rules

-

Geographic restrictions

-

Preset or customizable spending limits

Red flag: providers that only support basic freeze/unfreeze functionality without stronger expense management tools.

3. FX Fees and Multi Currency Support

FX pricing is important if your business operates internationally. Some virtual card providers may advertise low fees, but then quietly add large foreign transaction fees, hidden conversion spreads, or just feature poor exchange rates. This can quickly drain thousands from annual business spending.

The best virtual card solutions for global teams support:

-

Multiple currencies

-

Strong multi currency support

-

Transparent FX pricing

-

Stable settlement systems

-

Efficient international payments

For example, a Wise Business account may work well for companies managing supplier payments across different regions.

However, some newer virtual card programs, such as Halocard, which allow for USD denominated virtual card payments for SaaS and advertising, may be much better options.

Keep in mind that providers such as Halocard also provide users with a US-issued virtual credit card with a US BIN and US billing address, allowing for great acceptance, both in the USA and outside.

4. Accounting Software and Workflow Integrations

A great virtual card should not create any kind of accounting chaos. The best virtual corporate cards integrate directly with accounting software. This includes options such as QuickBooks and NetSuite, as well as other expense automation platforms.

If your organization relies heavily on existing accounting software, the quality of integration should be a top evaluation factor for you. Some providers focus heavily on approvals and automation, while others prioritize merchant acceptance and card issuance. Although neither is inherently better, which one you choose depends on your overall workflow.

Good integrations help:

-

Reduce manual data entry

-

Simplify reconciliation

-

Sync receipts automatically

-

Improve expense tracking

-

Help finance teams monitor transactions faster

Red flag: export-only workflows that still rely heavily on spreadsheets or other manual processes.

5. KYC and Onboarding Friction

Some virtual card providers might approve businesses within just minutes, whereas others can take weeks. The onboarding experience is important for founders, international businesses, remote teams, and companies operating across multiple entities.

Review:

-

Country availability

-

Business registration requirements

-

Verification timelines

-

Funding methods

-

Required documentation

There are providers that are more heavily optimized for US LLCs, whereas others are better for supporting global operators. For instance, a Wise Business setup might work smoothly for international transfers and vendor payments, but might not be ideal for every use case involving recurring SaaS subscriptions or advertising networks. By contrast, providers like Halocard are more readily accepted in the USA.

Red flag: unclear KYC requirements or sudden account freezes during onboarding.

6. Pricing Structure and Monthly Fees

Pricing for virtual cards can differ wildly depending on the provider.

Some providers charge:

-

Per-card fees

-

Platform fees

-

Percentage-based FX charges

-

Issuance fees

-

Decline penalties

-

Flat monthly subscription fees

Whereas other providers might rely primarily on interchange revenue or offer low cost or free tiers. The key here is knowing what the total operational cost is, not just the advertised monthly fee of the card.

For example, if your team plans on issuing many cards for subscriptions, departments, and contractors, pricing that is tied to volume can quickly add up. This is especially the case for businesses needing unlimited cards or large-scale virtual card programs.

Red flag: pricing pages that hide core operational fees until after signup.

7. Support Quality and Reliability

Finally, another important factor when deciding on a virtual card provider is support quality. If a billing issue interrupts your ad campaigns, payroll software, or infrastructure subscriptions, slow support can be a serious problem.

The best virtual card provider options offer:

-

Fast response times

-

Live chat

-

Clear SLAs

-

Strong documentation

-

Responsive mobile apps

-

Reliable uptime

Good providers also offer:

-

Real time visibility

-

Real time transaction monitoring

-

Instant alerts

-

Fast card replacement

-

Easy tools to monitor transactions and track failed charges

Red flag: support limited to email tickets with multi-day delays.

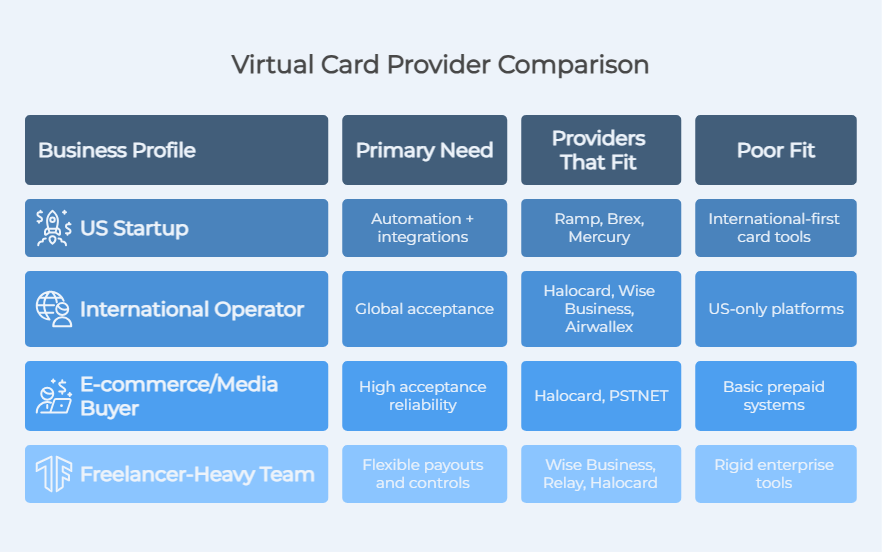

Which Virtual Card Provider Fits Your Business Profile?

Different virtual card solutions fit different operating models. There is no universal "best virtual credit card" for every company. It all depends on the company's needs.

| Business Profile | Primary Need | Providers That Fit | Poor Fit |

|---|---|---|---|

| US startup | Automation + integrations | Ramp, Brex, Mercury | International-first card tools |

| International operator | Global acceptance | Halocard, Wise Business, Airwallex | US-only platforms |

| E-commerce/media buyer | High acceptance reliability | Halocard, PSTNET | Basic prepaid systems |

| Freelancer-heavy team | Flexible payouts and controls | Wise Business, Relay, Halocard | Rigid enterprise tools |

US Startup

US startups generally prioritize workflow automation over card acceptance. Their biggest concerns are usually reimbursements, approvals, and syncing with accounting systems.

For these teams, modern corporate card platforms with strong integrations are often the best choice.

Various features such as automated approvals, receipt capture, and built-in expense tracking allow for streamlined operations and reduced overhead. This is where tools like Brex or Ramp are often chosen.

International Operator

For international operators, some of the most important factors to consider include flexible funding, merchant acceptance, and easy cross-border payments. Providers such as Halocard or Wise Business fit well here as they support broader international workflows and multiple funding methods.

Halocard is a solid choice as it is accessible in over 140 countries, and thanks to featuring a US BIN, it features strong acceptance in the USA.

E-Commerce or Media Buying Teams

E-commerce operators and media buyers need payment reliability. Declined cards disrupt subscription tooling, critical operational systems, and ad campaigns. Due to this, many e-commerce and media buying teams prioritize higher acceptance virtual credit cards over feature heavy automation tools. Again, options like Halocard are ideal, as they feature strong international acceptance.

This type of business also tends to require:

-

Fast card creation

-

Dedicated card details

-

Aggressive spending controls

-

High-volume vendor payments

-

Better management of ad spend

Freelancer-Heavy Teams

Companies that manage contractors across regions generally need flexible virtual card solutions for distributed spending across the globe.

The best setups usually combine:

-

Simple onboarding

-

Fast funding

-

Flexible payouts

-

Strong expense management

-

Clear spending limits

Some businesses may also prefer providers that support Google Pay, Apple Pay, and mobile-first workflows for employees that make occasional in store purchases or travel related expenses.

Red Flags When Evaluating Virtual Card Providers

Some warning signs appear repeatedly across weak virtual card platforms.

-

Hidden foreign transaction fees

-

Weak or non-existent support

-

Poor merchant acceptance rates

-

Unclear transaction fees

-

No advanced spending controls

-

Limited ability to track expenses

-

Weak integrations with accounting software

-

Delayed onboarding or frozen accounts

-

Disposable card instability

-

Poor mobile apps and unreliable alerts

You should also be cautious of providers that position themselves as enterprise-ready while lacking basic operational features like:

-

Expense tracking

-

Approval workflows

-

Reliable exports

-

Security alerts

-

Real-time controls

Shortlisting Process

Here is a process for shortlisting the best virtual card provider for your business.

Step 1: Define Your Core Use Case

Ask yourself, are you optimizing for employee reimbursements, vendor payments, international operations, or SaaS subscriptions? The fact is that different virtual card solutions specialize in different workflows.

Step 2: Compare the Real Pricing

Always compare the real pricing, not just the visible monthly fee. Always review issuance pricing, FX costs, decline fees, and any other hidden platform charges.

Step 3: Review Integrations

Review any integrations that you may need such as with ERP stacks, reimbursement workflows, and accounting systems.

Step 4: Test the Workflow

You should then test the workflow by creating sample cards, assigning permissions, and testing the actual payment process.

Step 5: Evaluate Support Responsiveness

Before making any final decision, contact the support team with a real operational question and then evaluate the response quality.

How to Pilot a Virtual Card Provider Before Committing

Before committing to any new virtual card for your business, you should run a controlled pilot.

Your checklist should include:

-

Test recurring online payments

-

Run real vendor payments

-

Create department-specific cards

-

Validate spending limits

-

Test freeze/unfreeze functionality

-

Review reporting and exports

-

Confirm real time visibility

-

Evaluate support speed

-

Monitor transactions for approval consistency

-

Test compatibility with your bank account workflows

Where Halocard Fits

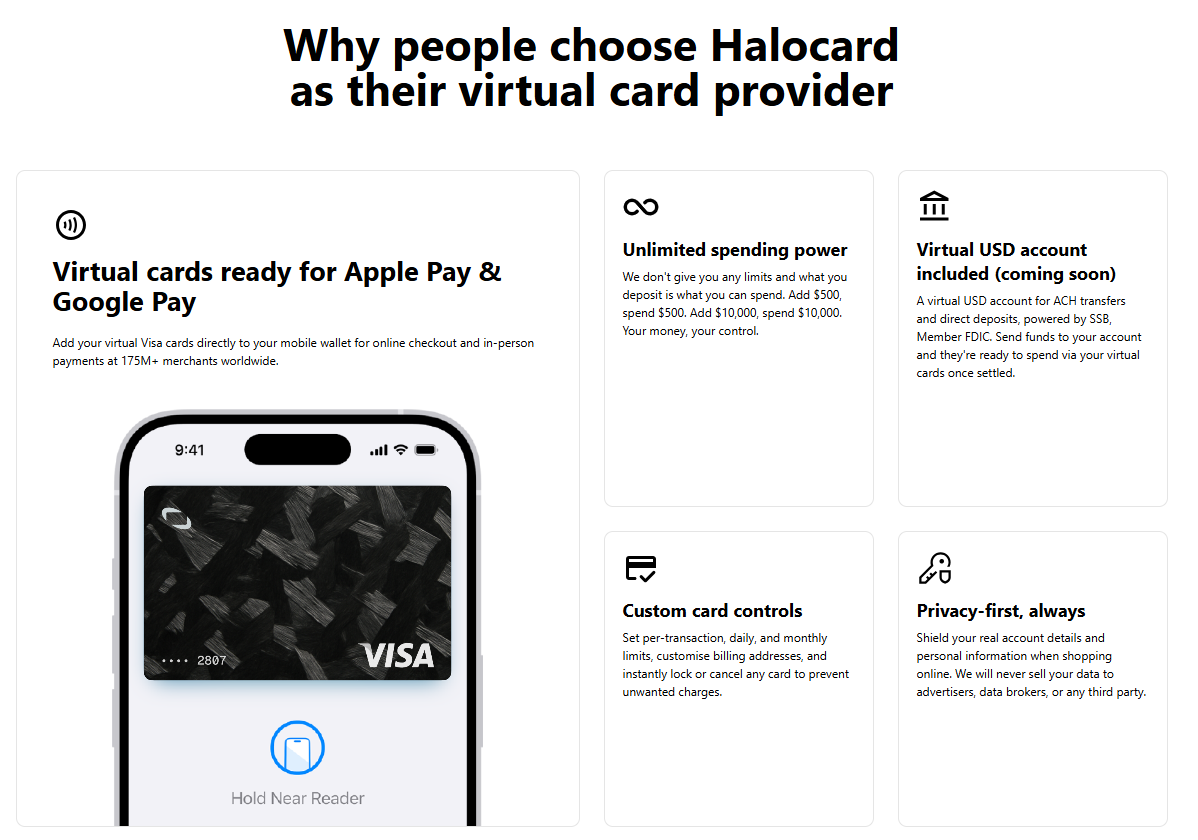

Halocard is best for businesses that prioritize global availability, merchant acceptance, and flexible funding over deeper enterprise automation. Halocard features a US-issued secured Visa structure, along with a US BIN and US billing address, which improves approval rates for SaaS tools, subscriptions, and many e-commerce transactions.

Halocard tends to see higher acceptance than prepaid cards and debit cards because it is a secured Visa, and US merchants generally accept it because it is US-issued.

Halocard is also ideal as it supports stablecoin funding, which helps businesses improve overall cash flow flexibility. With that being said, Halocard may not be the best fit for US startups that require deeply integrated expense management along with advanced accounting automation.

Frequently Asked Questions

What Is the Best Virtual Card Provider for Small Businesses?

The best virtual card provider for small businesses depends on what your operational priorities are. For instance, if you prioritize strong international acceptance and broad funding capabilities, Halocard may be best for you.

Are Virtual Credit Cards Better Than Physical Cards?

Generally speaking, virtual credit cards are better than physical cards for many types of online payments. Unlike physical cards, virtual cards reduce your overall exposure by allowing businesses to isolate vendors, create dedicated payment credentials, and even mask primary payment details.

Can Virtual Cards Replace Traditional Corporate Cards?

In many cases, yes, modern virtual corporate cards can replace traditional corporate cards, as they support reporting, approvals, expense tracking, and also feature advanced controls.

Do Virtual Cards Support Spending Limits?

Yes, the vast majority of virtual cards support spending limits, allowing businesses to engage in proper expense management.

Can Wise Business Be Used for Virtual Cards?

Yes, a Wise Business account can be used for virtual cards, and is especially useful for businesses that operate across multiple currencies.

Why Do Some Virtual Card Payments Get Declined?

Some virtual card payments get declined due to merchant restrictions, failed AVS checks, geographic blocks, expired card details, or unsupported prepaid infrastructure.

Are Virtual Corporate Cards Safe?

Yes, most modern virtual corporate cards are safe due to featuring strong security features, transaction alerts, and tools that help reduce unauthorized transactions from occurring.

Can Virtual Cards Improve Cash Flow?

Yes, virtual cards can improve cash flow by allowing businesses to better manage subscription cycles, payment timing, and approval workflows.

Sources

-

Reddit. Virtual Credit Cards for Your Vendors, What's a Good Solution? : r/msp

-

Priority Commerce. How to Choose the Best Virtual Business Credit Card | Priority Commerce

-

Airwallex. How to choose the best corporate card for your business

-

Stack Exchange. How can I select the best virtual credit card? - Personal Finance & Money Stack Exchange

-

Finextra. How to choose the best virtual card provider for your business: By Nikunj Gundaniya

-

WEX. How to choose the best virtual card provider: 3 essential tips | WEX Inc.

Sources checked on May 12, 2026.

*Please see Halocard's Terms of Service or Pricing for the most up to date pricing and fee information. This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Halocard LLC or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional. We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Halocard Virtual Cards

Instant approval

Create your first card in under 5 minutes.

Private purchases

Purchases never appear on your bank account.

Powered by Visa

Accepted at 175M+ merchants globally.

3 steps to create your virtual credit card

1. Sign-up with a phone

Sign up from your browser. No app download needed.

2. Quick identity check

Verify you're a real person in less than 3 minutes. No US residency required.

3. Add funds to your account

Use stablecoins, debit/credit card, or bank transfer (1%).

Your virtual card is ready.

That's it! Your virtual cards can now be used for online and in-person purchases anywhere in the world where Visa is accepted.