-

JCB works well in Japan, but it's not universally accepted and may not work on many international online platforms. If your Japanese card keeps failing on EU or US websites, the issue is often acceptance.

-

Japan has 3D Secure rules, and these matter for online shopping and subscription payment. Since 2025, debit card, credit card, and prepaid card products in Japan need stronger authentication for many online transactions.

-

Local prepaid card options like Kyash are convenient for domestic cashless payments, contactless payments, convenience stores, and everyday shopping. However, Japanese-issued cards can still be limited for overseas platforms.

-

A US-issued virtual card is generally the strongest option for Japanese residents who need international access, making the Halocard secured US-issued Visa card one of the strongest options.

If you live in Japan and your JCB card got declined on an international website, this is a common issue. Although JCB has great domestic coverage, and although many Japanese credit cards work perfectly in store and at department stores, as well as for local cashless payments, the issue generally arises when you try to pay for overseas subscriptions, ad platforms, or any kind of US based online shopping.

Even both MasterCard and Visa cards issued by Japanese banks sometimes fail internationally due to payment systems checking the card's issuing country, or due to billing address format, card type, or 3D Secure support. This guide compares the best virtual credit cards in Japan so Japanese residents can make international payments.

Quick Comparison Overview

| Provider | Type | Fees | Funding | Limits | Acceptance | Best For |

|---|---|---|---|---|---|---|

| Halocard | Virtual secured credit card with a US-issued Visa credit BIN | From $12/month or $1.25 per card. 0% fee on USD purchases, 1.5% FX fee on non-USD purchases. Stablecoin funding is free, while card funding has a 5% fee | Credit card, debit card, Apple Pay, Google Pay, stablecoins, or bank transfers in USD, EUR or GBP | No preset limit. You spend what you load, with per-card transaction, daily, and monthly controls | Excellent for international online shopping, US subscriptions, SaaS, ads, and merchants that prefer a US-issued credit card. Supports 3D Secure by Visa | Japan residents who need reliable US and international payment access, especially for ChatGPT, Claude, Netflix, SaaS tools, ad accounts, and US platforms |

| Kyash | Japan-issued Visa prepaid card and app-based virtual card | No monthly fee. Overseas service fee is 3%. Bank and Seven Bank ATM withdrawals are ¥220. Kyash Card issuance is ¥900 and Kyash Card Lite is ¥300 | Bank account, Seven Bank ATM, Lawson Bank ATM, convenience stores, Pay-easy, credit cards, debit card, and linked service points | Balance-based. Limits and available functions depend on account type and identity verification | Strong for domestic cashless payments, QUICPay, smartphone payments, and Japanese online shopping. Mixed for overseas platforms because it is a Japan-issued prepaid card | Users in Japan who want a convenient local prepaid Visa for domestic shopping, app payments, spending controls, and basic money management |

| V-preca | Japan-issued virtual Visa prepaid card from Life Card | No monthly fee. Digital issuance or purchase fees generally run about ¥200 to ¥290 depending on denomination. Physical card version costs ¥900. Dormancy fee of ¥125 may apply after three inactive months | Convenience stores, credit cards, bank account, gift codes, and pay-later top-up options | Balance-based. The newer V-preca can be recharged, but gift-style versions are better treated as one-off prepaid cards | Good for domestic online purchases and some international Visa merchants. Not ideal for recurring services, and some merchants with repeated monthly fees or ongoing billing may not accept it | One-off online purchases, users without regular credit cards, and people who want to avoid sharing their main card details |

| Wise | Physical multi-currency debit card for Japan residents. The Wise virtual card is not available to Wise accounts registered in Japan | No monthly fee. Japan-issued card ATM withdrawals are free for the first two withdrawals up to ¥30,000/month, then fees apply. Currency conversion usually starts from 0.73%, depending on currency | Wise account balance funded by bank transfer and supported local methods | Balance-based. You can spend what you hold across supported currencies | Strong for travel, transfers, and foreign currency spending. Not a true virtual card option for Japan residents, and not a credit card | Expats, freelancers, and travellers in Japan who need multi-currency spending, overseas transfers, and local ATM access, but not an instant digital-only card |

| Revolut | App-based multi-currency debit card with physical, virtual, and disposable virtual cards | Standard plan is free. Premium is ¥980/month and Metal is ¥1,980/month. Virtual and disposable virtual cards are free to issue. Some card top-ups, ATM withdrawals above ¥25,000/month, and FX activity outside fee-free limits may carry fees | Bank transfer, supported card top-ups, and Revolut account balance | Balance-based. Standard plan FX and ATM allowances apply by monthly cycle | Strong for travel, budgeting, app controls, and multi-currency spending. Less reliable than a US-issued credit card for some US merchants | Users in Japan who want a fintech account for travel, currency exchange, disposable cards, transfers, and everyday international spending |

| VANDLE Card | Japan-issued app-based Visa prepaid card | No enrollment fee and no annual fee. Basic virtual use is free. Pay-later "Pochitto Charge" has fees, age checks, and screening. Real card options may have separate fees | Convenience stores, internet banks, bank ATMs, credit cards, and Pochitto Charge | Balance-based. Users load money in advance, although Pochitto Charge can add funds instantly and collect payment later | Good for domestic online shopping, app purchases, subscriptions, Google Pay touch payments, and transport or smartphone payment top-ups. Limited for US platforms because it is a Japan-issued prepaid card | Younger users, people without traditional credit cards, and anyone wanting a fast no-credit-check prepaid Visa for everyday Japanese online use |

| PayPay Balance Card | Japan-issued virtual Visa card tied to PayPay Balance | Free to issue, no annual fee, and no traditional credit check. Standard online payments are deducted from PayPay Balance or eligible PayPay Points | PayPay Balance, PayPay Money, PayPay Money Lite, and eligible PayPay Points depending on settings | Balance-based. Transactions cannot exceed available PayPay Balance unless auto top-up is enabled | Strong for Japanese online shops that accept Visa. PayPay says it generally cannot be used at most overseas online shops, with some exceptions | PayPay users who want to use PayPay Balance for domestic Japanese online shopping, earn PayPay Points, and pay where direct PayPay checkout is not available |

Best Virtual Cards in Japan - Debit Card, Prepaid Card, and Credit Cards

Here are the top virtual cards in Japan that provide the best chances at being accepted internationally, including the number one pick, Halocard.

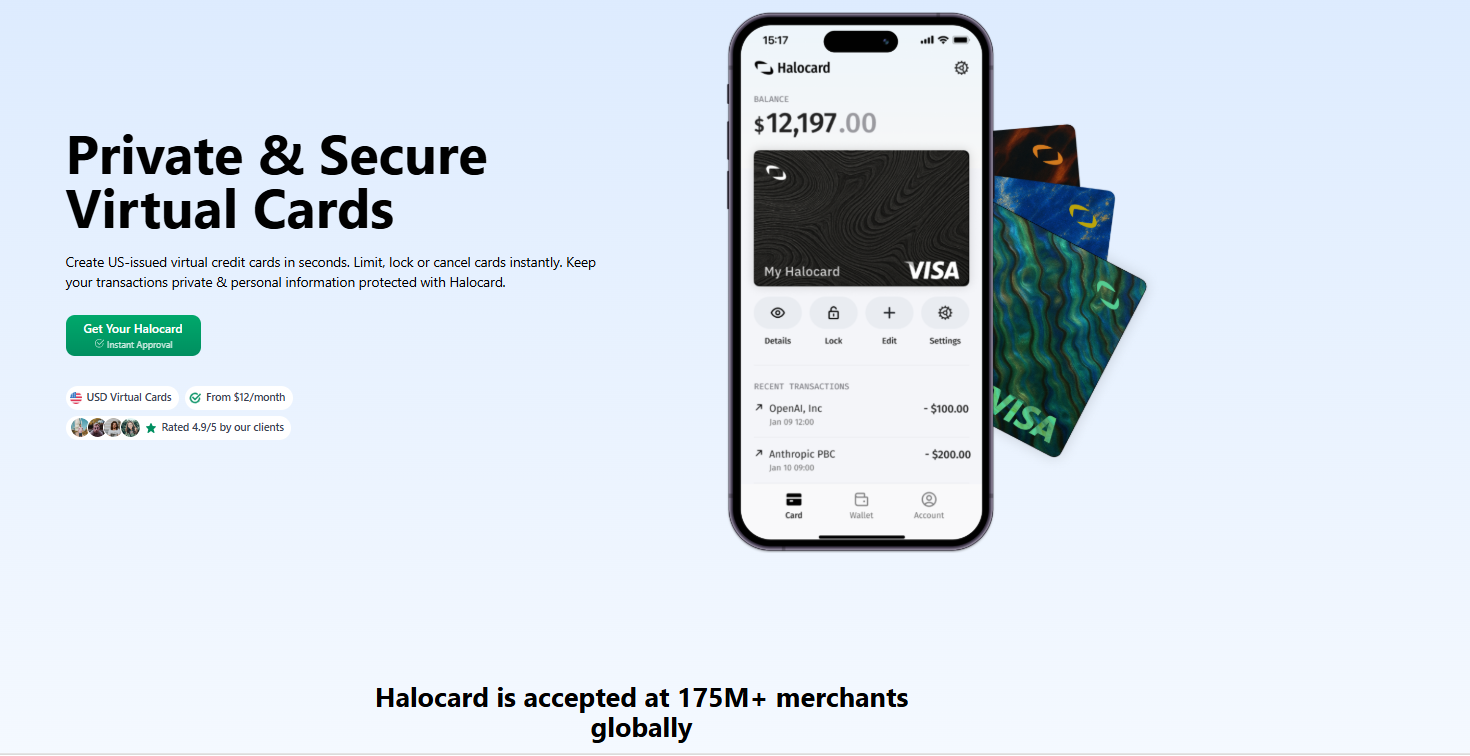

1. Halocard

Halocard is a US-issued secured Visa virtual card that is designed for subscriptions, ad spend, AI platforms, SaaS tools, online shopping, and various other international payment needs. For residents of Japan, the main advantage is that Halocard is not issued by a Japanese bank account or through a local credit card company. This means that it avoids many BIN and billing address issues that affect Japanese prepaid card, debit card, and credit card products.

At this time, Halocard is available in 144 countries. Non-US residents do not require an SSN, and there is no traditional credit check, allowing for easy access. Verification simply requires a national ID or passport, as well as a selfie. Once users are approved, residents can create a virtual card instantly and use it wherever Visa is accepted.

Halocard is secured, meaning that your spend is tied to the funds you load in advance, although the card is viewed as a secured credit card. Moreover, you can also set transaction limits, daily and monthly spending controls per card, lock cards instantly, and separate subscriptions across multiple cards.

Next, Halocard also supports 3D Secure by Visa, as well as various digital wallets, Google Pay, Apple Pay, and contactless payments where supported. A big benefit is that users can use whatever address feels the most comfortable being shared with the merchant. Overall, Halocard is the best option for Japanese residents who need to pay for services such as Netflix, Claude, ChatGPT, ad accounts, SaaS platforms, and various other overseas services that may not accept Japanese issued cards.

2. Kyash

Kyash is a simple and convenient local prepaid card in Japan. It issues a Japanese Visa card through its app, called the Kyash card virtual. This can be created in about a single minute and is ideal for online use. Simply load money in advance, spend from your balance, and then manage all payment activity from your phone or tablet.

Kyash can be funded through convenience stores, credit cards, bank accounts, debit card, and linked service points. This makes it convenient for users who need a prepaid card that fits Japan's existing cashless payments and cash habits.

Kyash is very useful for domestic online shopping, Google Pay, Apple Pay, smartphone payments, and contactless payments at stores. With identity verification, Kyash can also provide cashback or points style rewards, depending on the current program terms.

The app also features balance tracking, notifications, real time transaction history, card locks, usage limits, and controls for overseas and online payments. That said, the main limitation here is international reliability, as it is a Japanese issued prepaid card, not a US-issued credit card. This means that while it may work for some overseas merchants, it may still be declined by many US platforms that prefer a credit card, apply strict checks to foreign prepaid cards, or require a US billing address.

3. V-preca

V-preca is a Japanese issued Visa prepaid card designed mainly for online shopping. It's very useful if you need a virtual card for a single purchase, subscription, or a site where you don't want to enter your main credit card details. The card can be created in the app or browser, card number can then be used, along with the expiration date and security code, making it ideal for online use.

One of the biggest strengths of this card is its accessibility, as it does not require a credit check. Charge codes can then be purchased through credit cards, convenience stores, or bank accounts, as well as gift codes or pay later options. V-preca also supports Google Pay with the newer option being rechargeable, making it more flexible than a single-use gift-style prepaid card.

Now, the fees are worth noting, as issuance fees may range anywhere from ¥200 to ¥290, with the physical card costing up to ¥900. There is also a dormancy fee of ¥125 if the card is not used for three months. Acceptance is still a limitation here, as this is a Japanese issued prepaid card, so it may not be accepted at every merchant, particularly internationally. It's a useful card for one off online purchases, but certainly not the strongest option for US subscriptions and platforms that prefer credit cards, especially from the USA.

4. Wise

Wise is a good option for Japanese residents who need multi-currency spending, ATM access, low FX costs, and international transfers. Residents in Japan are able to open a Wise account, complete their identity verification, and order a Wise physical debit card.

Interesting to note is that although the Wise virtual card can be used in Japan when registered from a different country, it's not actually available to residents of Japan.

In fact, as of 2026, only the Wise physical debit card is available in Japan, but the Wise virtual card is not. In other words, the instant digital-only card that is generally created inside the app is not available for users with a Wise account that is registered in Japan. This is a very important limitation to note if you specifically require a virtual credit card option for instant online use.

With that being said, residents from many other countries can still access this virtual card and then use it in Japan. A benefit is that Wise fees are generally very transparent. Keeping all this in mind, Wise is best for freelancers, expats, and travelers who want efficient international payment, currency conversion, and transfers.

The main drawback is of course that it is mostly a physical debit card product in Japan, not a US-issued credit card or instant virtual card. This means that Japanese residents with a Wise account will still not be able to purchase online in the USA.

5. Revolut

Revolut is an international fintech option for people in Japan who need multi currency spending, international transfers, budgeting tools, and app based card controls. Revolut Japan offers a free standard plan as well as premium and metal plans. Revolut provides physical cards, virtual cards, and even disposable virtual card options.

Revolut is a convenient option for Japanese residents because users can exchange multiple currencies, create a virtual card in the app, get instant spending notifications, and manage funds from one single account. Moreover, the standard plan does not have a subscription fee, with Revolut saying that its virtual cards and disposable virtual cards are free to issue.

Another interesting note is that Revolut as a company is also registered in Japan as a Class 2 Funds Transfer Service Provider with the Director General of the Kanto Local Finance Bureau.

Next, the fees depend on how you fund and use your account, with the standard plan generally having the lowest usage limits before fees apply. Revolut is a useful option for budgeting, transfers, travel, and everyday international payment. That said, keep in mind that it is still a debit card product, not a US-issued Visa card or secured credit card, meaning that acceptance at US merchants is less reliable.

6. VANDLE Card

The VANDLE Card is a Japanese issued Visa prepaid card that users can create through the app in about just one minute. It's designed for people who want a simple virtual card for online shopping, subscriptions, app payments, and everyday cashless payments without applying for traditional credit cards.

The biggest advantage for residents of Japan is its accessibility, as you only need a phone number to start. There's also no credit check or strict screening process for the basic card. Moreover, there are also no annual fees, making it appealing for many. It's also appealing for people without a standard credit card or anybody who wants to easily control spend by loading money in advance.

The card can be loaded through convenience stores, internet banks, bank ATMs, and credit cards. It also features a pay later top up option for users 18 and older, although this does involve screening and fees.

The limitation of this card is similar to many of the others on the list, which is that this is a Japanese issued prepaid card, not a US-issued credit card. Although it generally works well for domestic online use, it's generally quite limited for international subscriptions and overseas use, particularly in the USA.

7. PayPay Balance Card

The PayPay balance card is one of the newest virtual cards out there, and it lets users spend their PayPay balance at Japanese online merchants that accept Visa. It's designed for those who already keep money in PayPay and want an extra way to pay at online shopping sites that may not support app checkout or direct PayPay QR.

Card issuance is free through the PayPay app, does not have any annual fees, and it doesn't require a traditional credit check. That said, prior identity verification through KYC is required. Once issued, card creation is nearly instant, with each transaction being deducted directly from your PayPay account.

The PayPay balance card is very useful for domestic cashless payments, Japanese websites, and users who already use PayPay.

However, once again, the limitation here is international acceptance. Even PayPay itself says that the card can generally not be used at most overseas online shops, with a few exceptions. So, it's a convenient option in Japan, but not a reliable solution for US subscriptions and international platforms.

How to Choose the Right Virtual Card

Here are a few important tips on how to choose the right virtual card in Japan.

For US Services and International Subscriptions

If you need to pay for US services, such as ChatGPT, Netflix, Claude, cloud platforms, ad accounts, or anything else from the USA, Halocard is generally the best option. It is a US-issued secured Visa credit card with a US BIN, US billing address, it supports 3D Secure by Visa, and it provides you with a custom billing address option. This generally helps solve the acceptance problem that often affects Japanese issued credit cards, debit cards, and prepaid cards.

For Domestic Japanese Online Shopping

If you need a card just for domestic Japanese online shopping, Kyash and PayPay are both fine options to consider. Both are Japan-focused, convenient, and built around local cashless payments, convenience stores, and everyday payment habits. Kyash is ideal if you want a broad app based prepaid card, whereas PayPay is best if you already have money in a PayPay account.

For Travel, Freelancing, and Multi-Currency Spending

If you're looking for multi currency spending for freelancing, travel, or overseas transfers, Revolut is the strongest fit. Although Wise was once a good option, due to the virtual card no longer being available to Japanese residents, it is no longer a viable choice.

For One-Off Online Purchases

If you're only looking to make single purchases, V-preca is the simplest choice. It's easy to use online, easy to fund, and does not require a traditional credit check.

Why Japanese Cards Get Declined on International Platforms

There are a number of reasons why Japanese cards may get declined on US and other international platforms.

JCB Is Strong in Japan, but Not Always Overseas

While JCB is a great option inside of Japan, as it's widely accepted by Japanese stores, and online shopping sites alike, its coverage outside the country is not very strong. Although some overseas merchants may accept JCB through network partnerships, most US and EU platforms still focus on MasterCard and Visa, meaning that JCB is often not accepted. Generally speaking, JCB is not accepted internationally, particularly in the USA.

Japanese-Issued Visa and Mastercard Cards Can Still Fail

The interesting note is that even MasterCard and Visa may fail on some US platforms when they originate from Japan. Many online processors and merchants use BIN country checks which identify the country where a card was issued.

If a system sees that a card was issued in Japan but the user is trying to buy a service that is US only, use a US billing address, or access a platform that has strict fraud rules, the transaction will most likely be blocked.

Address verification system checks can also cause issues because Japanese address formats generally don't match the structure that US systems expect. This means that even legitimate credit cards for major Japanese banks or major credit card companies may still be declined.

3D Secure Has Become a Bigger Requirement

3D Secure has become extremely important in Japan. As of 2025, Japan's online card security rules pushed ecommerce merchants to adopt 3DSecure 2.0, with online sellers in Japan expected to enable it by March 2025.

Generally speaking, online card payments in Japan must go through 3DS, and transactions without this authentication may be declined. This push is tied to the rising level of card fraud in Japan, with 92.5% of it linked to card-not-present-fraud, which is exactly what happens in online transactions.

Why Card Type Matters

Overall, card type matters greatly. A Japanese issued prepaid card may only work for domestic cashless payments, but for international subscriptions and US platforms, a US-issued card with a US BIN number and US billing address, along with 3D Secure support, is the more reliable choice.

Frequently Asked Questions

Why Is My Japanese Card Declined on International Websites?

Your Japanese card may be declined on international websites because the payment system flags in Japan issued MasterCard or Visa BIN, the billing address fails checks, or the card is not supported by 3DS. Japanese debit style and prepaid cards may also be denied, especially when compared to credit style cards.

Do Virtual Cards Work With 3D Secure in Japan?

Yes, some virtual cards work with 3D Secure in Japan, but this depends on the provider. For instance, Halocard supports 3D Secure by Visa.

Can I Use a Virtual Card to Pay for ChatGPT or Claude From Japan?

Yes, you can use a virtual card to pay for ChatGPT or Claude from Japan, however, Japanese issued cards may sometimes fail due to billing address mismatches, BIN country checks, or prepaid card restrictions. A US-issued virtual credit card that Japan residents can access, such as Halocard, is generally the most reliable option for US based subscriptions and platforms.

Do I Need an SSN to Get Halocard From Japan?

No, non-US residents do not require an SSN to get Halocard from Japan. Only residents of the USA require an SSN to get Halocard. There is also no traditional credit check involved.

What Is the Difference Between Prepaid, Debit, and Secured Credit Cards?

A prepaid card is loaded with money in advance and you can only spend what is available on the card. A debit card on the other hand is linked to an account balance and pulls funds from that account. Third, a secured credit card is backed by deposited funds but functions more like a real credit card, which can improve acceptance compared with many prepaid cards.

Can I Build US Credit History From Japan?

Yes, if you have a secured credit card, it may help contribute towards your US credit profile. This is especially the case if the provider reports activity to US credit bureaus. Keep in mind that prepaid card and debit card products do not build credit history.

Sources

-

Halocard. Instant, Private & Secure Virtual Cards | Halocard

-

Kyash. 選べる入金方法 - Kyash

-

Kyash. 障害・メンテナンス情報 - Kyash

-

V-preca. 会員規約|VisaプリペイドカードならVプリカ

-

V-preca. Vプリカのご利用方法|VisaプリペイドカードならVプリカ

-

V-preca. If you have a Visa prepaid card, you can use V-Preka

-

Wise. Can I get the Wise card in my country? | Wise Help Centre

-

Wise. Virtual Card | Create your Wise Virtual Debit Card - Wise

-

Wise. Does Wise work in Japan? Fees, ATMs, and how to use Wise in Japan - Wise

-

Revolut. About us | Revolut Japan

-

Revolut. Revolut | All-in-one finance app for your money | Revolut Japan

-

VANDLE. If it's a prepaid card, it's a bundle card|Visa card that can be made with an app

-

VANDLE. ポリシー | 株式会社カンム

-

VANDLE. 個人情報保護方針 | 株式会社カンム

-

VANDLE. 情報セキュリティ基本方針 | 株式会社カンム

-

VANDLE. バンドルカードについて – バンドルカード サポート

-

VANDLE. プリペイドカードならバンドルカード|アプリで作れるVisaカード

-

PayPay. Launch of Virtual Card "PayPay Balance Card"! | May 21, 2025 Press Release | PayPay Corporation

-

PayPay. PayPayを便利に使う - PayPay

-

PayPay. PayPayをはじめる - PayPay

-

PayPay. PayPay ヘルプ - キャッシュレス決済のPayPay

Sources checked on May 5, 2026.

*Please see Halocard's Terms of Service or Pricing for the most up to date pricing and fee information. This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Halocard LLC or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional. We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Halocard Virtual Cards

Instant approval

Create your first card in under 5 minutes.

Private purchases

Purchases never appear on your bank account.

Powered by Visa

Accepted at 175M+ merchants globally.

3 steps to create your virtual credit card

1. Sign-up with a phone

Sign up from your browser. No app download needed.

2. Quick identity check

Verify you're a real person in less than 3 minutes. No US residency required.

3. Add funds to your account

Use stablecoins, debit/credit card, or bank transfer (1%).

Your virtual card is ready.

That's it! Your virtual cards can now be used for online and in-person purchases anywhere in the world where Visa is accepted.