-

Virtual credit cards are generally safer than a physical credit card for online purchases because they hide your real card number from merchants.

-

Virtual cards are beneficial because they reduce exposure from data breach events, stolen credit card numbers, and risky subscription billing, but they do not stop every single type of fraud.

-

The level of safety depends on the virtual card provider, the card issuer, account security, dispute support, and controls.

-

Halocard can be very useful for international users who need a US-issued virtual credit card for safer and more reliable US merchant payments.

Yes, virtual credit cards are generally considered to be fairly safe for online spending, especially when compared to using your regular physical card. That said, they are, however, not magic.

A virtual card number can reduce damage if the merchant is breached, but it will, however, not protect you from account takeovers, phishing, or sending money to the wrong person. This guide explains exactly how virtual credit cards work, what they protect against, what they do not protect against, and how to choose a reliable virtual credit card provider with safety in mind.

How Virtual Cards Protect You

Virtual cards protect you in several ways, with the first main way having to do with isolated virtual credit card numbers.

Isolated Virtual Credit Card Numbers

The biggest piece of security that virtual card users have is separation. When you shop online, instead of entering your actual credit card number from your physical credit card, you enter a separate virtual card number for online transactions. This means that the merchant, and anybody else who might access the data, only sees virtual card details, not your real card details connected to your credit card account.

If that merchant happens to suffer a data breach, your exposed card number, expiration date, and security code may not give criminals access to your actual account. This is why using a virtual credit card is very useful when you shop online with new merchants, software tools, trial subscriptions, or international platforms.

The merchant still gets valid payment information, but your real credit card information stays protected. Some virtual credit card numbers are also created as randomly generated numbers tied to your real account number. Others are generated through a standalone virtual card provider. Either way, the goal is the same, which is to create an extra layer between the merchant and your real credit cards.

Merchant-Locked and Single-Use Virtual Cards

Some virtual cards can also be locked to a single merchant, meaning that the card number only works with that seller. If someone steals the card and tries to use it somewhere else, the transaction will be declined. There are also other virtual credit cards that are designed for one-time purchases.

Once the transaction is done, the virtual number is cancelled or expired. This is useful for short-term trials, unfamiliar stores, or just for merchants that you don't plan to shop at again.

For businesses, multi-use cards can be assigned to specific vendor payments, departments, subscriptions, and contractors. This is beneficial because it helps prevent misuse across multiple vendors and gives finance teams cleaner records for accounts payable transactions and other payable transactions.

Subscription Control and Spending Limits

Another great and practical security feature that digital credit cards have is spending limits. Instead of giving a merchant open-ended access to your main credit card account, you can set spending limits by day, month, merchant, or transaction. This is useful for subscriptions because you can cap the amount a merchant is allowed to charge you.

For example, if a free trial turns into a paid plan, or if a vendor unexpectedly increases pricing, the charge may fail if it exceeds your limit. For SMBs, these controls are also important for employee spending, expense management, approval workflows, and vendor payments.

A business can issue a variety of separate virtual cards for ad spend, contractors, and departments without sharing a main card number across the company.

No Physical Skimming Risk

Skimming is a big problem that physical cards faced, as they can be skimmed at ATMs, gas pumps, or compromised terminals.

However, a virtual credit card is different, because it does not have a plastic form to swipe, tap, or insert, so it avoids this risk. That said, this does not mean that virtual cards are always better for in person transactions. Some only work online, whereas others can be added to Google Pay, Apple Pay, Google Wallet, or even a phone's digital wallet for contactless payments. If this is the case, your digital wallet adds another layer of tokenized protection.

That said, the main safety advantage is online use. For the vast majority of people, virtual credit cards are best for online purchases, merchant-specific payments, and subscriptions, with a physical card remaining available for places that require a plastic card.

3DS, Wallets, and Built-In Controls

Many card issuers and credit card providers support added authentication tools such as 3D Secure, device verification, transaction alerts, and card verification checks. Some virtual cards also work with digital wallet tools such as Apple Pay and Google Pay, which also have their own built-in security features.

These features help reduce unauthorized use, particularly when combined with strong passwords and two factor authentication on your provider account. The most secure setup is generally a mix of a trusted financial institution or provider, unique virtual credit card numbers, wallet support, alerts, and strict spending limits.

What Virtual Cards Do NOT Protect Against

There are some things that virtual cards do not protect against, including the following.

Phishing

Unfortunately, a virtual card number will not protect you if you enter login details on a fake website. If a criminal happens to steal your actual credit card issuer account, digital wallet, or standalone provider account, they may be able to view, create, or use your virtual cards from within your account.

Account Takeover

On that note, if someone does get into your provider account, the issue is not just one stolen card number. They may actually access the account information, change settings, view virtual card transactions, or even create new credit card numbers that they will then use to make purchases. Device alerts, two factor authentication, and strong passwords are important.

Provider-Side Risk

In general, safety depends quite heavily on the card provider, with a weak virtual card provider offering poor support, unclear fees, limited dispute handling, or poor account controls. Keep in mind that not all card issuers offer the same protections, and not all standalone platforms are equally reliable.

Authorized Push Payment Fraud

If you willingly fund an account because of a scam, approve a transfer, or willingly send money, a virtual credit card will likely not save you. This type of fraud generally depends on deception rather than stolen credit card information.

Platform Account Fraud

A virtual credit card protects the payment layer, but not every single account connected to it. If someone hacks into your Google or Amazon account, they may still cause damage. Yes, the card number matters, but so do passwords, platform-level controls, and recovery e-mail security.

All Acceptance Problems

Some merchants may reject certain payment methods, especially debit cards, prepaid cards, cards with mismatched billing details, or international cards. A virtual credit card can be safer, but acceptance always still depends on the card issuer, BIN, network, billing address, and specific merchant rules.

Virtual Card vs Physical Card: Security Comparison

| Threat | Physical Card | Virtual Card |

|---|---|---|

| Merchant data breach | Real physical card number may be exposed | Separate virtual card number can be cancelled |

| Online merchant risk | Main card number is shared | Isolated card number is used |

| Skimming | Possible at compromised terminals | No plastic card to skim |

| Subscription overbilling | Harder to control | Spending limits and merchant controls may help |

| Lost or stolen card | Plastic card can be used physically | No physical object to steal |

| Credit card fraud disputes | Usually covered by issuer policies | Often has the same fraud protection, depending on issuer |

| In person transactions | Widely accepted | Depends on digital wallet support |

| Business vendor payments | Often one shared card | Separate cards for vendors and teams |

Yes, virtual credit cards are safer for online shopping, business payments, and subscriptions because they reduce the overall exposure of your real credit card numbers. That said, a physical credit card is still fairly useful for broad acceptance, especially when it comes to in person transactions. The safest setup is not necessarily one or the other, but both together, a regular credit card for daily use, and digital credit cards for riskier online payments.

How to Evaluate a Virtual Card Provider

Here are a few things that you need to know about how to evaluate a virtual credit card provider in terms of overall safety and other features.

Check the Card Network and BIN

Check if the card is a Visa, MasterCard or on another network. You must also ask yourself if it is a debit, prepaid, secured credit, or actual credit card. These details all affect acceptance rates.

For example, Halocard issues a US-issued secured Visa virtual credit card, which helps international users who need US merchant acceptance. This is important because many US merchants and networks will not accept virtual credit cards from international sources, particularly if the BIN is from another country, or if it is a prepaid or debit card. Your best chance of acceptance is a US-issued credit card with a US BIN and billing address, such as Halocard.

Review Spend Controls and Merchant Rules

A good virtual card provider should always let you control the card. This means you should have access to spending limits, merchant-level controls, transaction caps, cancel or instant lock options, and transparency into each transaction.

For businesses, the provider should also support practical controls for expense management, employee spending, vendor payments, and recurring software payments. The controls should be granular, as more granular controls help reduce risk.

Understand the Chargeback and Dispute Process

Good credit cards aren't just useful because they help you pay, but because they also come with dispute rights. Before signing up, check how a credit card issuer or provider handles failed deliveries, unauthorized charges, merchant disputes, or duplicate charges. If the provider is vague about dispute handling or support, be careful. Safety is about what happens after something goes wrong, not just about preventing fraud in the first place.

Look at Account Security

In terms of account security, at the very least, the provider account should support two factor authentication, secure login, transaction notifications, quick card freezing, and device alerts. A safe virtual credit card provider should make it easy to spot unusual activity, and even easier to stop it quickly. You should also check how your account information is handled. KYC is very normal for financial products, but the provider should always explain what data it collects, why, and what happens with it.

Confirm Regulatory Standing and Transparency

Perhaps most important of all, a trustworthy virtual credit card provider should clearly explain its fees, issuing partners, limits, card type, terms, and funding methods. Established fintechs, major banks, and transparent standalone platforms tend to be quite safe compared to anonymous sites that sell instant card access with little detail. Established credit card providers and major issuers may offer strong protections, but not all card issuers provide flexible virtual credit card numbers. Standalone options can be very useful, especially for international users, but that said, provider quality does matter.

Frequently Asked Questions

Are Virtual Credit Cards Safer Than a Physical Credit Card?

Yes, virtual cards are generally safer for online use than a physical credit card. The reason for this is that they let you use a separate card number instead of exposing your real credit card numbers to every single merchant that you shop at. This reduces the overall damage from a data breach, suspicious merchant, or any kind of unwanted recurring charge. That being said, they are not a full replacement for strong account security.

Can a Virtual Credit Card Number Get Hacked?

Unfortunately yes, a virtual credit card number can be stolen, but the damage is generally much easier to contain. You can usually delete, freeze, or replace the virtual card number without replacing your actual credit card. If the number is merchant locked or capped with spending limits, it will also be much less useful to a criminal or hacker.

Do Virtual Credit Cards Affect My Credit Score?

Usually, virtual credit cards affect your credit only through the underlying account. If the virtual credit card is tied to an existing credit card account, the normal balance and payment behavior do make a difference. Individual virtual card transactions usually do not create separate credit lines, so always check with your card issuer if you are not sure.

Can I Use Virtual Cards for Subscriptions?

Yes, virtual cards are great for subscriptions, because you can create a separate card number, set a low limit, or even cancel the card when you no longer require the service. This prevents surprise renewals, accidental upgrades, or merchants that make cancellation very difficult.

Can I Shop Online With Digital Credit Cards?

Yes, you can shop online with many digital credit cards, anywhere the network and card type are accepted. All you have to do is enter the card number, expiration date, and security code like you would with any other normal card. Some virtual credit cards can also be added to a digital wallet for mobile checkout.

Do Virtual Credit Card Numbers Protect Against Identity Theft?

Virtual credit card numbers do help protect your banking information, although they do not fully protect against identity theft. A stolen card number is not the same as stolen identity documents, bank credentials, or passwords. For the highest level of security, use a virtual credit card along with strong passwords, two factor authentication, credit monitoring, and careful document handling.

Do Virtual Cards Have the Same Fraud Protection as Regular Credit Cards?

Generally speaking, yes, virtual cards have the same fraud protection as regular credit cards, although this depends on the card issuer. Bank issued virtual credit cards usually have the same dispute and fraud rules as the underlying account, whereas standalone platforms may vary, so always check the terms before relying on any provider for business payments or major purchases.

Can International Users Get a Virtual Credit Card for US Merchants?

Yes, many international users can get a virtual credit card through standalone platforms. For instance, Halocard is designed for users who need a US-issued Visa card without a US SSN. This can be helpful for SaaS tools, US subscriptions, ad platforms, and for other merchants that may reject non-US credit cards or prepaid payment methods.

Sources

-

Reddit. Are virtual cards a good option for securing your online purchases? : r/CreditCards

-

JPM. What is a Virtual Credit Card and How Does It Work? | J.P. Morgan

-

Bankrate. Is It Safe To Add A Credit Card To My Digital Wallet | Bankrate

-

Chase. How Virtual Credit Card Numbers Protect Your Information | Chase

-

USBank. Virtual Account Protection

-

CNET. Fraud-Proof Your Online Purchases: Why Virtual Cards Are Your New Best Friend - CNET

Sources checked on May 6, 2026.

*Please see Halocard's Terms of Service or Pricing for the most up to date pricing and fee information. This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Halocard LLC or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional. We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Halocard Virtual Cards

Instant approval

Create your first card in under 5 minutes.

Private purchases

Purchases never appear on your bank account.

Powered by Visa

Accepted at 175M+ merchants globally.

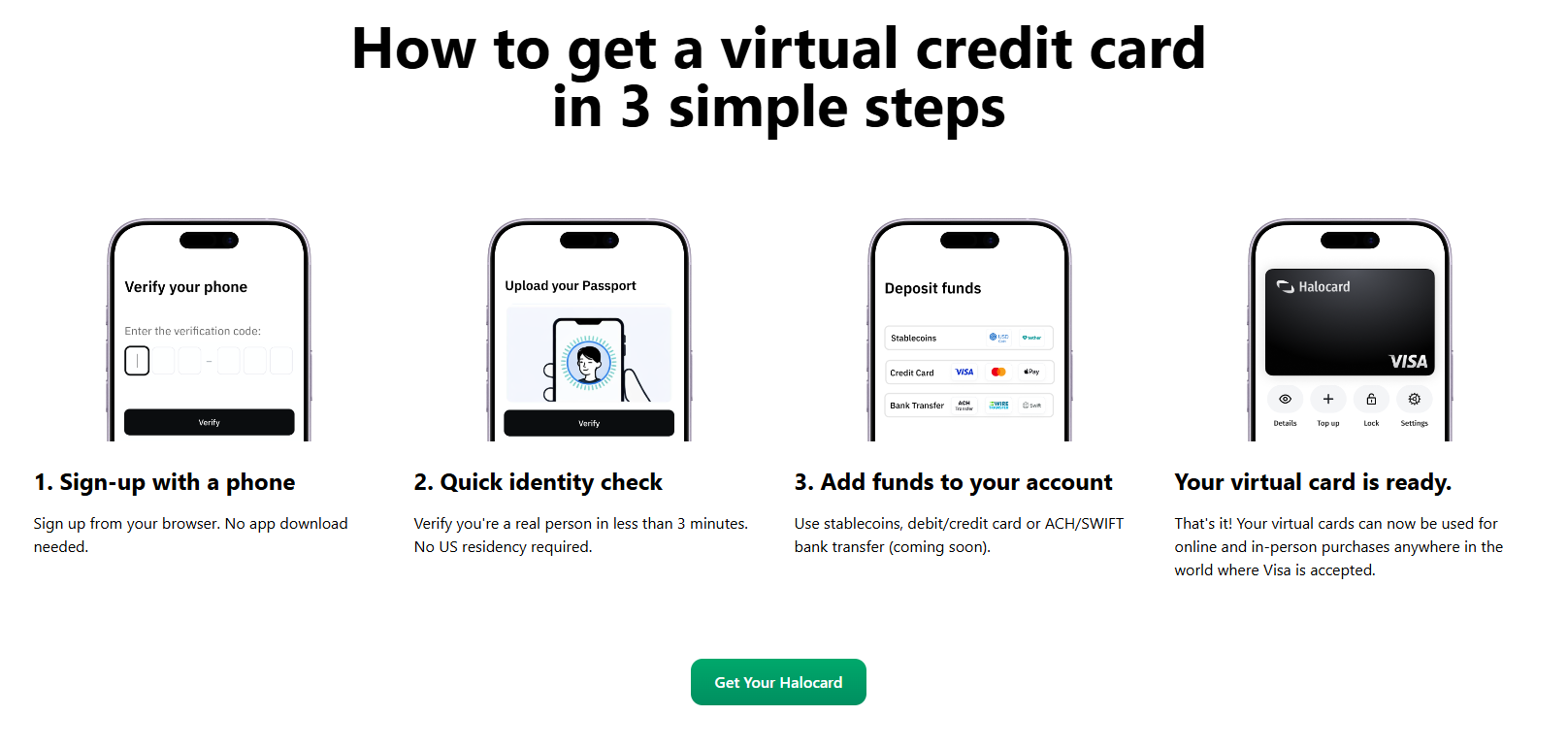

3 steps to create your virtual credit card

1. Sign-up with a phone

Sign up from your browser. No app download needed.

2. Quick identity check

Verify you're a real person in less than 3 minutes. No US residency required.

3. Add funds to your account

Use stablecoins, debit/credit card, or bank transfer (1%).

Your virtual card is ready.

That's it! Your virtual cards can now be used for online and in-person purchases anywhere in the world where Visa is accepted.