Benefits of Virtual Cards Over Physical Cards for Company Expenses

Edward Taylor

-

Waiting for a physical card can often take days or weeks, whereas virtual cards can be issued instantly for immediate use.

-

With virtual cards, businesses get tighter spending controls with per-card merchant restrictions, subscription-specific limits, and employee caps.

-

Unlike physical corporate cards, virtual cards help reduce exposure to skimming, physical theft, and various forms of unauthorized transactions.

-

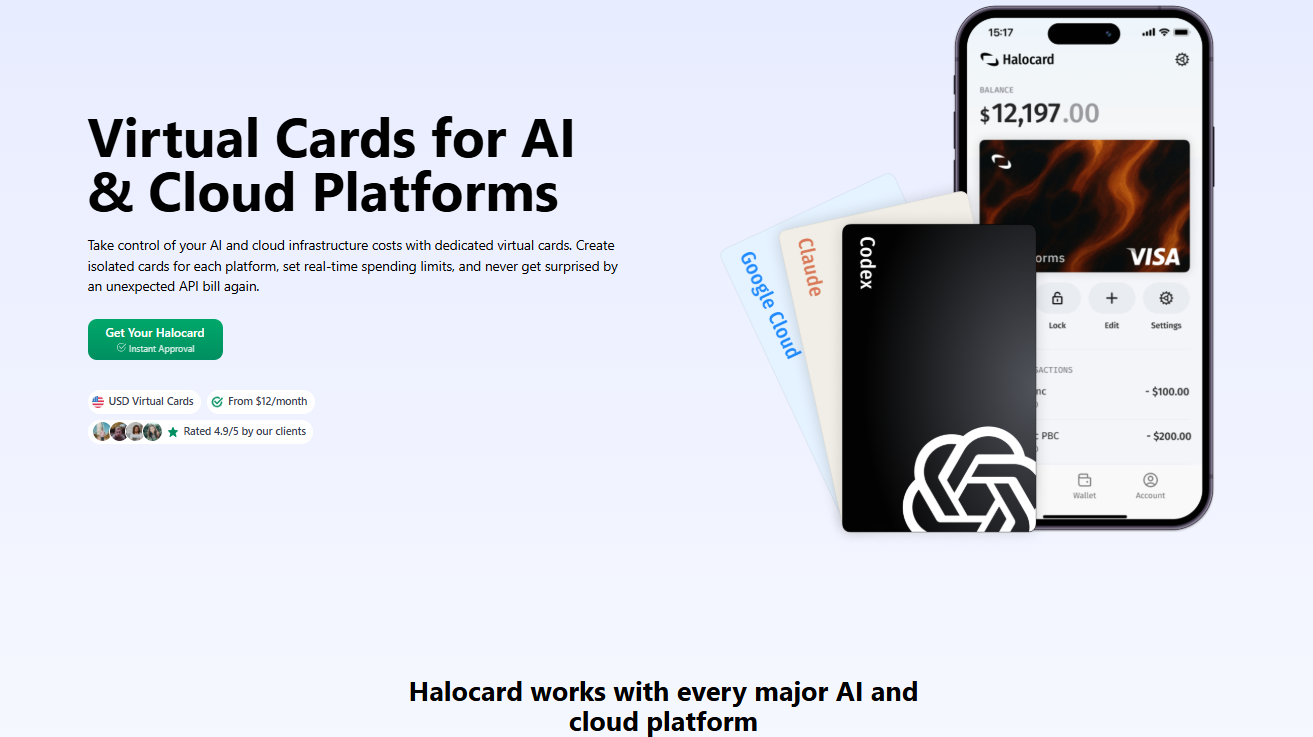

Halocard stands out as a top option for international teams because it provides users with US-issued Visa access with very strong acceptance for ad platforms, SaaS, and online payments, both within and outside the USA.

Physical corporate cards worked well when most employees sat in a single office, made the occasional purchase, and submitted a pile of paper receipts at the end of the month. Modern businesses move much faster, with teams being remote, software subscriptions stacking up quickly, and business expenses happening across many platforms every single day.

Because of this shift, many companies are replacing or supplementing physical corporate cards with virtual credit cards. Virtual cards change how businesses control spending, manage fraud exposure, and track transactions. Instead of giving employees a reusable plastic card that is directly tied to broad company budgets, finance leaders can now create payment credentials for specific vendors, subscriptions, or employees, in mere seconds.

Physical Corporate Card vs Halocard Virtual Card Comparison

| Feature | Halocard Virtual Card | Traditional Physical Corporate Card |

|---|---|---|

| Card Type | Digital-first virtual credit card platform | Standard physical credit card program |

| Privacy & Security | Strong security with merchant-specific cards and instant lock/cancel features | Higher exposure to card cloning, loss, and physical theft |

| Acceptance | US-issued secured Visa credit card with strong US merchant acceptance for SaaS and ad platforms | Widely accepted for in person transactions and travel |

| Availability | Instant issuance globally in 144 countries | Often limited by country residency and banking requirements |

| Funding Options | Stablecoins, ACH, debit/credit card funding | Primarily bank-linked |

| Spending Controls | Granular spending limits, vendor locks, and transaction caps | Usually broader account-level controls |

| Reissue Process | Create replacement cards instantly | Requires shipping a new physical card |

| Best For | Remote teams, SaaS subscriptions, vendor payments, ad spend, and international businesses | Frequent travel, hotels, and heavy in person purchases |

Key Differences Between Virtual and Physical Corporate Cards

Let's take a closer look at the primary difference between virtual cards and physical corporate cards.

Issuance Speed and Employee Onboarding

One of the biggest immediate benefits of virtual cards is speed. Finance teams are able to instantly create virtual cards for contractors, new employees, or vendors without waiting for physical cards to ship.

With traditional corporate cards, onboarding generally means a lot of paperwork, approvals, shipping logistics, and activation steps. A virtual card provider such as Halocard allows businesses to issue cards in minutes and begin using them right away.

Spending Controls and Budget Management

Virtual cards allow businesses to set spending limits per employee or vendor. Regular credit cards generally rely on broad account-level credit limits. That doesn't work well when employees share spending authority.

Modern virtual and physical cards differ heavily in how they approach control, as virtual platforms restrict purchases to specific merchants, limit recurring subscription charges, control transaction size and frequency, and block categories unrelated to business-related expenses.

These spending controls greatly improve overall expense management and allow businesses to avoid surprise charges. For example, a company buying Facebook ads can create a single dedicated card for advertising spend and another for office supplies. If either of the vendors suffers a breach, the rest of the business remains isolated.

Fraud Exposure and Security Features

If you lose a physical credit card, there is an immediate risk. Someone who finds it or steals it can use it for fraudulent purchases, tap it for contactless payments, or even clone it through compromised terminals.

A virtual credit card greatly reduces that surface area because it primarily exists online, with no physical object to skim or steal. Virtual cards also help improve security because businesses can instantly cancel, pause, or replace credentials. Instead of freezing an entire company account after some suspicious activity, finance teams can isolate only the affected card.

This becomes important for subscription-heavy companies. If one service experiences a breach, businesses that are using dedicated virtual cards can just disable that card without interrupting unrelated business operations.

Real-Time Tracking and Reconciliation

With physical credit cards, manual reimbursement workflows are nothing but headaches. Employees use their personal cards, submit receipts later, and finance teams then spend hours matching charges to expense reports. Virtual cards simplify this process through automated categorization and built-in tracking.

Most platforms support real-time transaction tracking, faster reconciliation process workflows, cleaner exports into enterprise resource planning software, easier subscription management, and better visibility into employee spending. This leads to much more accurate credit card statements and much better cash flow oversight. This helps improve budgeting accuracy and supports overall company financial health.

Reissue Costs and Operational Friction

Replacing a compromised plastic card can be very disruptive, as employees will likely need to update recurring billing details across multiple vendors, wait for the card to ship, and even temporarily pause spending activity.

That said, virtual cards help avoid many of these issues, as businesses can instantly create cards, rotate compromised credentials, replace expired cards, prevent delayed payments, and continue operations without having to wait for a physical card to be delivered.

This kind of flexibility is very important for fast-moving digital businesses because failed subscription renewals can interrupt customer support, advertising, and access to critical infrastructure.

International Access and US Merchant Compatibility

International businesses often struggle with traditional methods. Non-US companies often face payment failures with ad platforms. This is also the case with subscription services and SaaS providers. This is because their local credit cards use BINs that are non-US, have debit classifications, or address mismatches.

Halocard solves this problem because it provides a US-issued Visa credential designed for global users. It features a US BIN as well as a US billing address, making it very useful for businesses that need reliable access to US merchants while operating internationally. For companies making online purchases across multiple countries, this can remove an operational bottleneck.

What Users Say About Virtual vs Physical Corporate Cards

Generally speaking, user sentiment around virtual and physical cards is quite consistent. For the most part, businesses prefer virtual cards for recurring software costs, distributed teams, and advertising spend. Many finance managers regularly mention major advantages such as better visibility into business payments, stronger spending controls, and streamlined expense management.

Many users also appreciate how easy it is to separate vendors or departments into dedicated cards, therefore simplifying reporting processes and reducing overall reimbursement chaos. Discussions often highlight the convenience of being able to assign separate cards to temporary workers or contractors without exposing broader company funds.

That said, users also point out real limitations, as virtual cards are not perfect for every use case. For example, some travel providers, rental car services, and hotels still require or prefer a physical card for deposits and verification. Point-of-sale terminals also struggle with manually entered virtual credentials during in person transactions. Due to this, many businesses use a hybrid setup that uses both virtual and physical payment methods together.

Physical Cards vs Halocard: Why Halocard Is the Winning Option

Let's take a look at why Halocard is the winning option when compared to physical cards.

Global Availability Without US Residency

Most providers restrict access based on geography. However, Halocard supports users in 144 countries without requiring a US SSN or US address (for non-US users).

Strong US Merchant Acceptance

Because Halocard is a secured credit card operating on the Visa network, which is issued in the USA, and includes both a US billing address and United States BIN, it has strong acceptance in the USA and internationally.

Instant Card Creation

Unlike physical debit or credit cards which can take days or even weeks to ship, with Halocard, businesses can instantly create virtual cards for campaigns, employees, or vendor payments without shipping delays. These cards can be used immediately.

Granular Spending Controls

Virtual cards such as Halocard also feature strong granular spending controls that help companies better manage spending and reduce unnecessary costs. For example, Halocard allows businesses to set transaction caps, limit employee budgets, control recurring billing, and restrict merchant categories.

Better Fraud Isolation

Virtual cards such as Halocard also offer better fraud isolation. Businesses can easily disable one card rather than shutting down an entire account, and this level of isolation is one of the key benefits that modern virtual cards offer.

Cleaner Expense Management

Dedicated cards are great because they simplify accounting workflows and reduce reimbursement overhead. This helps improve overall expense management systems, makes it easier to track spending across departments, and simplifies audits.

Flexible Funding Options

Another benefit of virtual cards such as Halocard is that it supports ACH, debit card, credit card, and stablecoin funding. This kind of flexibility is ideal for international teams that handle cross-border operations.

Honest Caveat: Physical Cards Still Matter Sometimes

Despite all of the advantages, physical cards can still be important. For instance, employees who travel a lot may still need a traditional card for rental vehicles, hotels, and some local purchases. Businesses that frequently handle in person purchases may also benefit from keeping a limited number of physical corporate cards active alongside their virtual systems.

How To Compare Virtual Card Providers for Business

Here are the most important factors you should keep in mind when comparing virtual card providers for business.

-

US merchant acceptance rates

-

International availability

-

Funding methods

-

Per-card spending controls

-

ERP and accounting integrations

-

Fraud prevention tools

-

Subscription management capabilities

-

Ease of reconciliation

-

Support for digital wallet payments

-

Pricing and FX fees

These are all of the factors that matter when evaluating virtual cards. On that note, Halocard is one of the strongest options for international businesses that need reliable US payment acceptance and flexible controls.

Frequently Asked Questions

What Are the Main Benefits of Virtual Cards Over Physical Cards?

The main advantages of virtual cards over physical cards are that they allow for faster issuance, tighter spending controls, improved fraud protection, and easier tracking.

What Is the Main Difference Between a Virtual Credit Card and a Physical Credit Card?

The main difference is that a virtual credit card is a digital payment credential that exists primarily online, whereas a physical credit card is a tangible card that can be used for both online and in person payments.

Do Virtual Credit Cards Work for Vendor Payments and SaaS Subscriptions?

Yes, virtual cards are useful for recurring software tools, subscription billing, and cloud infrastructure, because businesses can isolate vendors into dedicated credentials.

Are There Disadvantages to Virtual and Physical Cards?

Yes, some disadvantages of virtual cards are that they can struggle with car rentals, certain in person transactions, and hotels. On the other hand, physical credit cards may not be accepted internationally.

Can Virtual Credit Cards Be Added to Apple Pay or Google Pay?

Yes, many virtual card providers support both Apple Pay and Google Pay, as well as other mobile wallet platforms for tap-to-pay functionality.

How Fast Can Businesses Create Virtual Cards?

Businesses can create virtual cards almost instantly, making onboarding simple and fast.

What Happens if a Virtual Card Is Compromised?

If a virtual card is compromised, businesses can immediately cancel, pause, or freeze the affected card. Unlike physical cards, companies don't need to shut down the entire account after suspicious activity.

Are Virtual Cards Better for Expense Management Systems?

Yes, virtual cards are generally better for expense management systems as they improve real-time expense tracking, reduce manual reimbursement workflows, and simplify reconciliation.

Sources

-

Reddit. Virtual vs Physical card? When to use one or another? : r/Revolut

-

Reddit. Should I use my virtual or my physical card to pay with Apple Pay in physical stores? : r/Revolut

-

Reddit. Do you still use physical business cards, or have you gone fully digital? : r/Entrepreneur

-

Reddit. Are digital business cards actually better than paper ones? : r/smallbusiness

-

Airwallex. Virtual Card vs. Physical Cards: Which Comes Out on Top? | Airwallex CA

-

Float Financial. Physical vs. Virtual Corporate Cards: Pros & Cons | Float

-

Stampli. Virtual Cards vs. Physical Cards: Which is Better for Your Business?

-

Order. Virtual Card vs. Physical Card: Pros & Cons for a Virtual-First Strategy | Order.co

-

Wallester. Virtual Cards vs. Physical Cards: What's Better for Business? | Wallester

-

Instarem. Virtual business cards vs traditional bank cards: What businesses need to know

Sources checked on May 6, 2026.

*Please see Halocard's Terms of Service or Pricing for the most up to date pricing and fee information. This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Halocard LLC or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional. We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Halocard Virtual Cards

Instant approval

Create your first card in under 5 minutes.

Private purchases

Purchases never appear on your bank account.

Powered by Visa

Accepted at 175M+ merchants globally.

How to get a virtual credit card in 3 simple steps

1. Sign-up with a phone

Sign up from your browser. No app download needed.

2. Quick identity check

Verify you're a real person in less than 3 minutes. No US residency required.

3. Add funds to your account

Use stablecoins, debit/credit card or ACH/SWIFT bank transfer (coming soon).

Your virtual card is ready.

That's it! Your virtual cards can now be used for online and in-person purchases anywhere in the world where Visa is accepted.